April 2, 2026

How To Source Construction Chemical At Lowest Cost During War ?

What Is the Impact of the US-Iran War on Construction Chemical Prices and Availability ? The US-Iran conflict that escalated...

The Impact of the US-Iran War on Building Material Prices in 2026

The US-Iran conflict that escalated in early 2026 has sent shockwaves through the global economy – but nowhere are the effects more acutely felt than in the Middle East’s building material markets. From steel and cement to ceramics, construction chemicals, and PVC products, prices are shifting weekly, supply chains are fracturing, and importers across the Gulf face unprecedented uncertainty.

This is not a localized disruption. It is a regional crisis affecting every building material importer from Dubai to Dammam, from Doha to Kuwait City, from Muscat to Manama. Understanding the price impacts – and what you can do about them – is essential for protecting your business and your projects.

The Strategic Context : Why This Conflict Matters for Building Materials ?

The Middle East accounts for approximately one-third of global oil production. Iran is a significant regional producer of steel, cement, and petrochemical-based building materials. The Strait of Hormuz – through which 20% of global oil and 30% of LNG passes – is a chokepoint for bulk carrier traffic carrying building materials to and from the region.

When conflict erupts in this neighborhood, every input cost in construction moves.

| Strategic Factor | Impact on Building Materials |

|---|---|

| Oil prices | Primary input for plastics, PVC, chemicals, and transport fuel |

| Gas prices | Energy input for steel, aluminum, ceramics, and cement |

| Shipping routes | Hormuz disruption affects bulk carrier movement |

| Insurance costs | War risk premiums spike for all Gulf-bound cargo |

| Currency volatility | Regional currencies under pressure; import costs rise |

| Supply chain diversion | Rerouting adds time and cost to every shipment |

| Iranian supply gap | Regional supplier of steel, cement, petrochemicals disrupted |

Global Trade Context : The Ripple Effects Beyond the Region

The US-Iran conflict does not exist in isolation. It interacts with existing global trade tensions, shipping disruptions, and economic pressures to create a compound effect on building material prices.

Red Sea Shipping Crisis Continues

Even before the US-Iran escalation, the Red Sea shipping crisis – ongoing since late 2023 – had already rerouted significant traffic away from the Suez Canal. Houthi attacks on commercial vessels forced major carriers including MSC, Maersk, and Hapag-Lloyd to divert ships via the Cape of Good Hope, adding 14 – 20 days to transit times and 30 – 50% to shipping costs.

The US-Iran conflict now compounds this by threatening the alternative route through the Strait of Hormuz, leaving few safe passages for Gulf-bound cargo.

Global Shipping Capacity Under Pressure

| Factor | Current Status |

|---|---|

| Container vessel availability | Tight; new vessel deliveries lagging demand |

| Bulk carrier fleet | Aging fleet; limited new builds |

| Crew availability | Ongoing shortages post-pandemic |

| Port congestion | Global phenomenon; Gulf ports now added |

| Equipment imbalances | Containers stranded; repositioning costs high |

Energy Market Volatility

Brent crude surged past $90 per barrel in the immediate aftermath of the conflict escalation, with analysts projecting potential spikes to $120 – 150 if Hormuz shipping is significantly disrupted. Every $10 increase in oil prices adds approximately:

Inflationary Pressure Across Economies

Global inflation, which had been gradually moderating through late 2025, is now reignited by energy price spikes. Central banks face renewed pressure to maintain or raise interest rates, affecting construction financing and project viability.

Read More About GCC’s Building Materials Product Range

Regional Trade Impact : The Numbers Behind the Crisis

Middle East Building Material Trade Volumes

| Trade Flow | Annual Volume | Primary Products |

|---|---|---|

| Asia to GCC imports | ~45 million tonnes | Steel, ceramics, hardware, chemicals |

| GCC intra-regional trade | ~15 million tonnes | Cement, rebar, blocks |

| Iranian exports to region | ~5 million tonnes | Steel, cement, petrochemicals |

| Total at risk | ~65 million tonnes | All building material categories |

Strait of Hormuz: The Critical Chokepoint

A prolonged closure or significant disruption would require rerouting all Gulf-bound cargo through a combination of :

| Alternative Route | Impact |

|---|---|

| Red Sea (if safe) | Requires Bab el-Mandeb passage; also under threat |

| Mediterranean overland | Ship to Turkey, truck through Syria/Iraq – high risk, high cost |

| East Coast ports | Ship to Oman’s Salalah or Sohar, truck across UAE – adds time and cost |

| Air freight | Economically unviable for most building materials |

Read More About GCC’s Construction Chemical Range

Immediate Price Impacts by Product Category

1. Steel and Metal Products

Steel is the most sensitive building material to conflict-driven price volatility. The reasons are multiple and compounding.

Global Steel Market Context :

| Factor | Impact on Steel Prices |

|---|---|

| Iranian supply disruption | Iran exports ~110,000 tonnes of steel monthly to regional markets; this supply has effectively halted |

| Energy cost pass-through | Steel production requires 4 – 5 MWh per tonne; oil and gas price spikes raise costs globally |

| Shipping cost increase | Bulk carriers face higher insurance and longer diversions; freight rates up 40 – 60% |

| Scrap price volatility | Turkish and regional mills reliant on scrap face input cost swings; scrap prices up 15 – 20% |

| Freight route changes | Cape of Good Hope routing adds 14 – 20 days, tightening vessel availability and raising rates |

| Chinese export dynamics | China may redirect exports as other markets become more attractive |

Price Impact by Steel Product :

| Product | Typical Price Range (Pre-Conflict) | Current Estimate | Increase |

|---|---|---|---|

| Hot-rolled coil | $550 – 600/tonne | $660 – 750/tonne | 20 – 25% |

| Rebar | $530 – 580/tonne | $610 – 670/tonne | 15 – 18% |

| Steel plates | $580 – 630/tonne | $670 – 730/tonne | 16 – 20% |

| Structural sections | $600 – 650/tonne | $690 – 750/tonne | 15 – 18% |

| Galvanized sheet | $650 – 700/tonne | $780 – 850/tonne | 20 – 22% |

Current Outlook : Steel prices across the GCC have risen 15 – 25% since the conflict escalated, with further increases expected as inventory depletes and replacement costs reflect higher shipping and insurance. Analysts project sustained elevation through Q3 2026 at minimum.

2. Cement and Clinker

Cement is heavy, low-value, and regionally traded – but the conflict disrupts even these local dynamics. The cement market is particularly sensitive to energy costs and transport availability.

Regional Cement Market Context :

| Factor | Impact on Cement Prices |

|---|---|

| Energy cost pass-through | Cement production requires 60 – 130 kWh per tonne; fuel oil and electricity costs rising 15 – 20% |

| Transport cost increase | Trucking and coastal shipping both affected by fuel prices; diesel up 20 – 25% |

| Iranian supply gap | Iran was a significant clinker exporter to Gulf markets (UAE, Kuwait, Qatar); supply now halted |

| Infrastructure project demand | Government projects continue across KSA, UAE, Qatar, sustaining demand despite price pressure |

| Shipping constraints | Bulk cement carriers face same Hormuz risks as other vessels |

Price Impact by Market :

| Market | Typical Price (Pre-Conflict) | Current Estimate | Increase |

|---|---|---|---|

| UAE | $45 – 55/tonne | $50 – 63/tonne | 12 – 15% |

| Saudi Arabia | $50 – 60/tonne | $55 – 70/tonne | 10 – 16% |

| Qatar | $55 – 65/tonne | $62 – 75/tonne | 12 – 18% |

| Kuwait | $48 – 58/tonne | $53 – 67/tonne | 10 – 15% |

| Oman | $52 – 62/tonne | $58 – 71/tonne | 11 – 16% |

Current Outlook : Cement prices have increased 10 – 18% across the region, with coastal markets facing the largest increases due to shipping disruptions. Import-dependent markets like Qatar and UAE are most exposed.

3. PVC, Plastics, and Polymer-Based Products

PVC pipes, fittings, profiles, and other plastic building materials are directly linked to oil and gas prices. The petrochemical supply chain is among the most disrupted by the conflict.

Global Plastics Market Context :

| Factor | Impact on PVC/Polymer Prices |

|---|---|

| Feedstock price surge | Naphtha, ethane, and other petrochemical feedstocks track oil prices; up 25 – 30% |

| Iranian petrochemical exports | Major regional supplier disrupted; Iran exported significant PVC to GCC markets |

| Shipping container shortage | Container vessels rerouted; equipment imbalances worsen; container availability down 15 – 20% |

| Packaging cost increase | Every building material shipment requires packaging; plastic wrapping, straps, pallets all cost more |

| European energy crisis | European PVC production (linked to gas prices) remains constrained, limiting alternative supply |

Price Impact by Product :

| Product | Typical Price (Pre-Conflict) | Current Estimate | Increase |

|---|---|---|---|

| PVC pipes (pressure) | $1,200 – 1,500/tonne | $1,500 – 1,950/tonne | 25 – 30% |

| PVC fittings | $1,800 – 2,200/tonne | $2,300 – 2,900/tonne | 28 – 32% |

| PVC profiles (windows/doors) | $1,500 – 1,800/tonne | $1,900 – 2,400/tonne | 27 – 33% |

| WPC boards | $600 – 800/tonne | $720 – 1,000/tonne | 20 – 25% |

| PVC foam boards | $700 – 900/tonne | $840 – 1,150/tonne | 20 – 28% |

Current Outlook : PVC and plastic building material prices have surged 20 – 33%, with the most significant increases in imported finished goods. The combination of feedstock costs, Iranian supply gaps, and container logistics creates sustained upward pressure.

4. Ceramics, Tiles, and Sanitaryware

These energy-intensive products face compound pressure from natural gas prices and shipping costs. The ceramics industry is among the most energy-intensive in construction.

Global Ceramics Market Context :

| Factor | Impact on Ceramics Prices |

|---|---|

| Natural gas prices | Primary energy input for firing (800 – 1,200°C); European gas prices up 30 – 40%, Asian LNG prices following |

| Shipping costs | Fragile goods require careful container loading; freight rates up 30 – 50%; breakage risk increases with longer transits |

| Iranian production | Regional competitor supply disrupted; Iran produced ~500 million sqm annually |

| Chinese shipping routes | Longer transits via Cape of Good Hope increase breakage risk and insurance costs |

| Packaging costs | Cardboard boxes, plastic straps, edge protectors all cost more |

Price Impact by Product :

| Product | Typical Price (Pre-Conflict) | Current Estimate | Increase |

|---|---|---|---|

| Floor tiles (porcelain) | $8 – 12/sqm | $9 – 14/sqm | 12 – 18% |

| Wall tiles (ceramic) | $5 – 8/sqm | $5.60 – 9.50/sqm | 12 – 19% |

| Sanitaryware (WC) | $40 – 80/unit | $45 – 96/unit | 12 – 20% |

| Sanitaryware (basins) | $25 – 50/unit | $28 – 60/unit | 12 – 18% |

| Natural stone | $30 – 80/sqm | $33 – 92/sqm | 10 – 15% |

Current Outlook : Tile and sanitaryware prices have increased 12 – 20%, with delivery timelines extended by 3 – 4 weeks. Natural gas prices remain the primary concern for continued escalation.

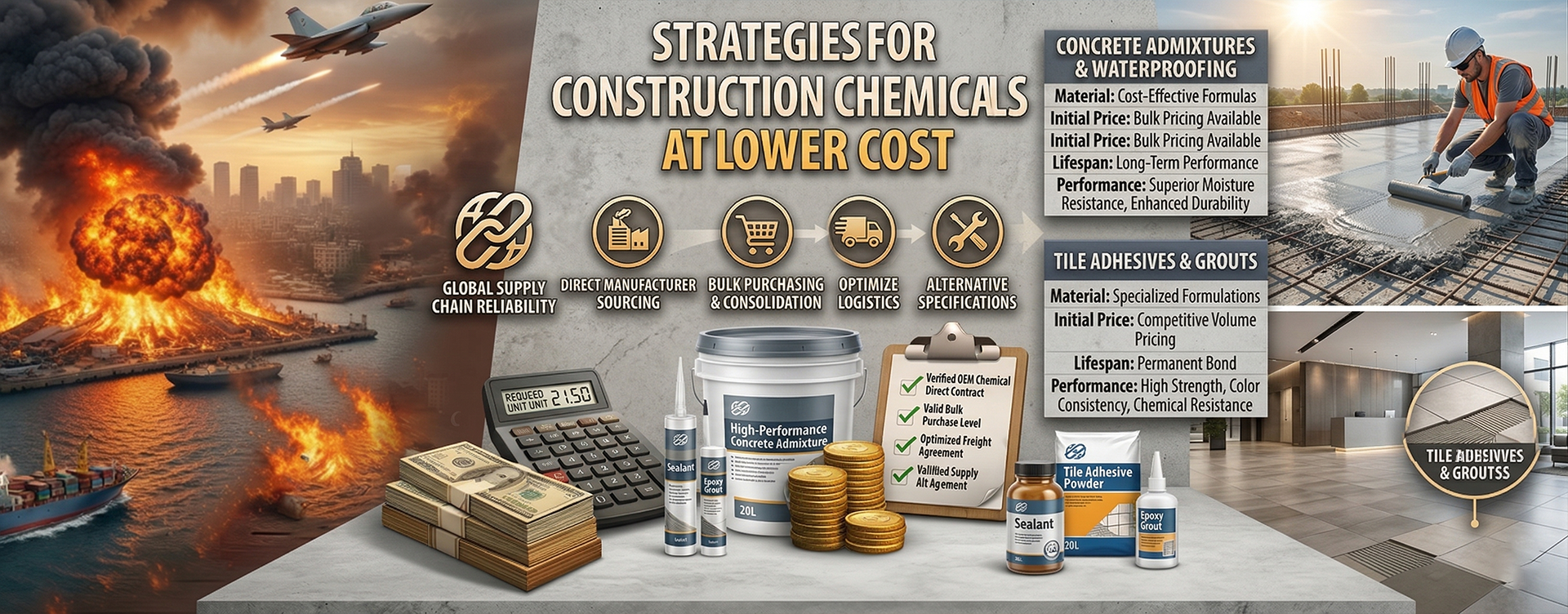

5. Construction Chemicals

Waterproofing compounds, tile adhesives, grouts, sealants, and repair mortars are petrochemical-intensive and face unique logistics challenges.

Global Construction Chemicals Market Context :

| Factor | Impact on Construction Chemicals |

|---|---|

| Petrochemical feedstock | Direct link to oil and gas prices; epoxy, polyurethane, acrylics all petroleum-derived |

| Hazardous shipping restrictions | Tighter regulations; fewer carriers willing to transport chemicals; documentation requirements increase |

| Insurance surcharges | Higher premiums for chemical cargoes; war risk adds 50 – 100% |

| Packaging costs | Plastic drums, pails, and containers cost more; steel drums also affected by steel prices |

| Specialty raw materials | Many additives and modifiers sourced from limited global suppliers; logistics chains disrupted |

Price Impact by Product :

| Product | Typical Price (Pre-Conflict) | Current Estimate | Increase |

|---|---|---|---|

| Waterproofing (liquid membrane) | $3,500 – 4,500/tonne | $4,000 – 5,400/tonne | 15 – 20% |

| Tile adhesive | $400 – 600/tonne | $460 – 720/tonne | 15 – 20% |

| Epoxy grout | $2,500 – 3,500/tonne | $3,000 – 4,200/tonne | 18 – 22% |

| Concrete admixture | $1,200 – 1,800/tonne | $1,400 – 2,200/tonne | 16 – 22% |

| Polyurethane sealant | $4,000 – 5,000/tonne | $4,800 – 6,200/tonne | 18 – 24% |

Current Outlook : Construction chemical prices have risen 15 – 24%, with the largest increases in solvent-based and hazardous formulations. Supply availability is as significant a concern as price.

6. Laminates, Plywood, and Wood Products

While less directly energy-intensive, these products face indirect pressure from shipping costs and resin prices.

Global Wood Products Market Context :

| Factor | Impact on Wood Products |

|---|---|

| Shipping costs | Container rates up 30 – 50%; space prioritization affects lower-value wood products |

| Resin costs | Adhesives and binders (urea-formaldehyde, phenol-formaldehyde) are petrochemical-derived; up 20 – 25% |

| Transport fuel | Land transport costs rising; last-mile delivery more expensive |

| Packaging materials | Plastic wrapping and edge protection cost more |

| Logistics delays | Moisture risk during extended transit; longer voyages increase damage claims |

Price Impact by Product :

| Product | Typical Price (Pre-Conflict) | Current Estimate | Increase |

|---|---|---|---|

| Marine plywood | $600 – 800/cbm | $650 – 900/cbm | 8 – 12% |

| HPL laminates | $2.50 – 4.00/sqm | $2.70 – 4.50/sqm | 8 – 12% |

| Compact laminates | $30 – 50/sqm | $33 – 56/sqm | 10 – 12% |

| Shuttering plywood | $500 – 700/cbm | $550 – 800/cbm | 10 – 14% |

| MR grade plywood | $400 – 550/cbm | $430 – 620/cbm | 8 – 12% |

Current Outlook : Laminate and plywood prices have increased 8 – 14%, primarily driven by shipping and resin costs. Further increases expected if oil prices remain elevated.

7. Furniture Hardware

Hardware products face pressure from shipping costs, raw material prices, and generalized inflation.

Global Hardware Market Context :

| Factor | Impact on Hardware Prices |

|---|---|

| Shipping costs | Container rates up 30 – 50%; hardware is volume-efficient but still affected |

| Raw material costs | Steel, aluminum, zinc prices rising 15 – 25% |

| Packaging | Plastic components and blister packs cost more; cardboard boxes up 10 – 15% |

| Labor costs | Inflation pressures in manufacturing economies; wages rising |

| Electronics components | Soft-close and electronic hardware affected by semiconductor supply chains |

Price Impact by Product :

| Product | Typical Price (Pre-Conflict) | Current Estimate | Increase |

|---|---|---|---|

| Hinges (stainless) | $1.50 – 3.00/pc | $1.60 – 3.30/pc | 5 – 10% |

| Handles/knobs (zinc) | $2.00 – 5.00/pc | $2.20 – 5.50/pc | 5 – 10% |

| Soft-close mechanisms | $5.00 – 12.00/pc | $5.50 – 13.50/pc | 8 – 12% |

| Drawer slides | $8.00 – 20.00/set | $8.80 – 22.00/set | 8 – 10% |

| Locksets | $10.00 – 30.00/pc | $11.00 – 33.00/pc | 8 – 10% |

Current Outlook : Furniture hardware prices have increased 5 – 12%, with premium finishes and electronic components facing larger increases. Shipping delays are as significant as price increases.

8. Disposable and Paper Products

Paper napkins, foodservice packaging, and disposable tableware serve the hospitality and construction camp sectors.

Global Paper Market Context :

| Factor | Impact on Disposables Prices |

|---|---|

| Pulp prices | Energy-intensive to produce; up 10 – 15% |

| Shipping costs | Container rates up 30 – 50% |

| Packaging | Plastic wrapping costs more |

| Freight prioritization | Lower-value goods face space competition |

Current Outlook : Disposable product prices have increased 8 – 12%, with further pressure expected.

Summary Table : Price Impact by Product Category

| Product Category | Price Increase (Estimated) | Primary Driver |

|---|---|---|

| Steel (HRC, plates, sections) | 15 – 25% | Energy + Iranian gap + shipping |

| Cement | 10 – 18% | Energy + transport fuel |

| PVC and plastics | 20 – 33% | Feedstock + Iranian petrochemical gap |

| Ceramics and tiles | 12 – 20% | Natural gas + shipping |

| Sanitaryware | 12 – 20% | Natural gas + shipping |

| Construction chemicals | 15 – 24% | Petrochemicals + hazardous shipping |

| Laminates and plywood | 8 – 14% | Shipping + resin costs |

| Furniture hardware | 5 – 12% | Shipping + raw materials |

| Disposables and paper | 8 – 12% | Pulp + shipping |

Read More About GCC’s Granite, Marble & Sandstone Range

Beyond Direct Prices : Secondary and Tertiary Impacts

Shipping and Insurance Costs

| Factor | Current Impact |

|---|---|

| Container freight rates (Asia-Gulf) | Up 30 – 50%; $2,500 – 3,500 per FEU depending on origin |

| Bulk carrier rates | Up 40 – 60% due to longer voyages and risk surcharges |

| War risk insurance | Premiums up 50 – 100% for Gulf-bound cargo |

| Transit time | Extended 14 – 20 days via Cape of Good Hope |

| Port congestion | Delays adding 7 – 14 days at major Gulf ports |

| Demurrage and detention | Costs rising as delays extend |

Currency and Financing

| Factor | Impact on Importers |

|---|---|

| Gulf currencies | Pegged to USD; stable but import costs rising in real terms |

| Egyptian pound | Continued pressure; import financing difficult |

| Jordanian dinar | Stable but tourism revenue affected |

| Letters of credit | Harder to open; banks more risk-averse; collateral requirements up |

| Payment terms | Suppliers demanding shorter terms; advance payments requested |

| Working capital | Extended timelines tie up cash; financing costs rising |

| Hedging costs | Currency and commodity hedging more expensive |

Project and Pipeline Impacts

| Factor | Consequence |

|---|---|

| Project delays | Materials unavailable or delayed; timelines slip 3 – 6 months |

| Cost overruns | Fixed-price contracts under pressure; renegotiations common |

| Bid inflation | New tenders pricing in 15 – 25% uncertainty buffers |

| Government spending | Potential reprioritization of infrastructure budgets |

| Private sector caution | Investment decisions postponed; new projects delayed |

| Contractor viability | Margins squeezed; some contractors at risk |

| Claims and disputes | Force majeure claims increasing |

Looking Ahead : Price Forecast Scenarios

| Scenario | Price Outlook | Timeline |

|---|---|---|

| Short-term conflict (1 – 3 months) | Prices spike 15 – 25%, then stabilize; gradual normalization | Q2 2026 |

| Medium-term conflict (3 – 12 months) | Sustained elevation at 15 – 30% above pre-conflict; structural supply changes | Through 2026 |

| Extended conflict (12+ months) | Permanent price reset at 20 – 35% higher; new supply chains emerge | 2027 onward |

| Escalation (Hormuz closure) | Immediate 30 – 50% spike; potential shortages | Any time |

The most likely path is medium-term disruption with permanently elevated price levels at 15 – 25% above pre-conflict baselines. Importers who treat this as a temporary problem will be caught off guard. Those who adapt will build lasting advantage.

Conclusion: Navigating the New Price Reality

The US-Iran conflict of 2026 has fundamentally altered building material prices across the Middle East. Steel is up 15 – 25%. PVC has surged 20 – 33%. Cement, tiles, and chemicals are all moving higher. Shipping costs have doubled in some lanes. Insurance is a new line item. Transit times are measured in months, not weeks.

Yet within this challenge lies opportunity. Importers who adapt – who diversify suppliers, consolidate shipments, build strategic inventory, and choose the right sourcing partners – will not only survive this period but emerge stronger, with more resilient businesses and better customer relationships.

The key is recognizing that the old normal of fragmented, transactional sourcing is suspended. The new normal demands partnership, consolidation, and strategic thinking. It demands partners who take responsibility, not those who pass risk.

Global Connect Corporation : Your Partner for Reliable, Cost-Effective Sourcing

Global Connect Corporation (GCC) is a direct supply partner with complete accountability – we supply, ship, and deliver building materials from Asia to importers across the Middle East at reliable and cost-effective prices.

| GCC at a Glance | |

|---|---|

| Verified Manufacturing Units | 200+ across Asia |

| Export Shipments Executed | 500+ |

| Countries Supplied | 12+ across Middle East and beyond |

| Product Categories | Complete building material portfolio |

| Operational Model | Direct supply; end-to-end accountability |

All shipments are executed under GCC’s export management, documentation, and payment framework, ensuring consistency, compliance, and reliability. GCC does not operate as a marketplace or agent – we supply, ship, and deliver with complete accountability.

Citations & Market References :

0

0

0

0 0

0 0

0